The BritCard Digital ID Psyop | A Bait and Switch

OffGuardian.org | Kit Knightly

Iain Davis | IainDavis.com

Apparently, in order to be able to work in the UK, we will all be forced to adopt digital ID—the mandatory so-called BritCard. There is absolutely no public appetite for this, as the more than 2 million and rising (at the time of writing) signatures to the online petition to stop it demonstrates.

Of course, online petitions don’t make any difference to governments, but at least they illustrate to us that government propaganda, such as the IPSOS poll that alleges 57% of the UK public want digital ID, is garbage. Though given IPSOS enormous number of government contracts, including its contract to assist in the design of the BritCard, willingly fulfilling its propaganda role is understandable.

Proudly announcing mandatory digital ID at the Global Progress Action Summit, Keir Starmer said:

Let me spell that out. You will not be able to work in the United Kingdom if you do not have Digital ID. It’s as simple as that.

This all sounds very “authoritarian,” but if we decide we are not going to adopt the BritCard, and if the UK government insists on enforcing it, the entire UK economy and the government will collapse. If government issued digital ID is “mandatory” to work in the UK, and millions, perhaps tens of millions, of people decide they are not going along with it, then that means mass unemployment, a vanishing government tax take, and economic destruction on a cataclysmic scale.

The government can be as tough as it likes, but if we tell it to do one there is sweet FA it can do about it. The government only has power while we comply, if we don’t it has absolutely none at all. It’s a paper tiger. We have all the power, we just have to realise it by not complying.

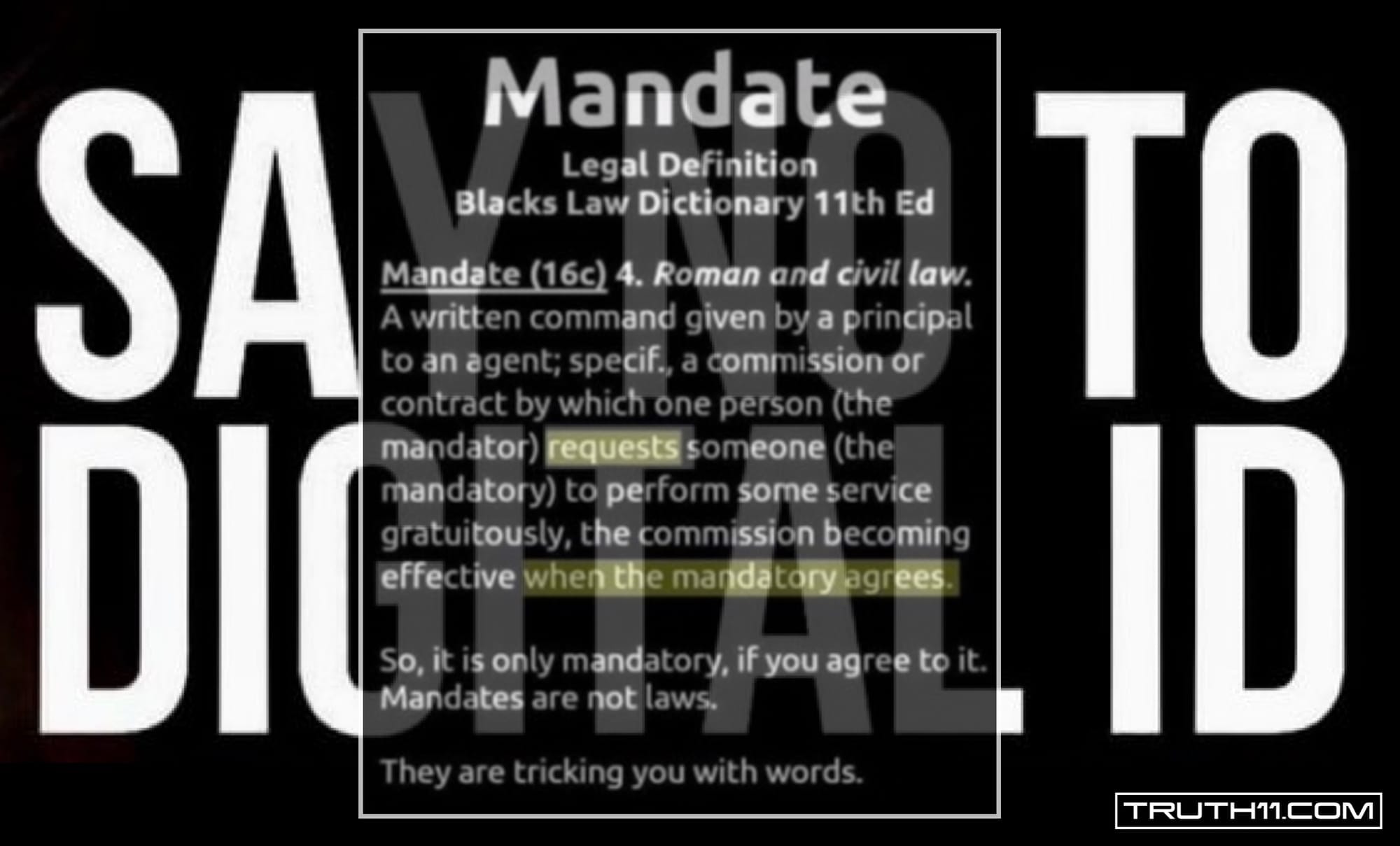

Clearly, there is no need for a UK digital ID. In a moment of stupidity, the UK Secretary of State for Culture, Media and Sport, Lisa Nandy, told the BBC that the national ID card would be the same as a national insurance number (NIN), insofar as you won’t be able to work without one. It didn’t occur to her that having a NIN is indeed a prerequisite for employment in the UK and, therefore, no one needs a government digital ID. Assuming, that is, the government’s claimed justification is remotely plausible. Which it isn’t

The government has exploited illegal immigration as an excuse to supposedly introduce digital ID:

[Digital ID] will [. . .] be required for right to work checks to stop those with no right to be in the country from finding work. This is to send a clear message that if you come here illegally, you will not be able to work, deterring people from making dangerous journeys.

There are few glaring problems with this ludicrous argument.

For a start, you can’t get a NIN if you are in the UK illegally. Those who employ people illegally couldn’t care less whether you have a NIN or not, just as they won’t care if a slave labourer has a BritCard or not. No “message” will be sent because those who come here illegally do so knowing it is illegal and the BritCard won’t make any difference to them either. Nor will trafficked illegal immigrants be deterred because they don’t have a choice and the traffickers show no signs of giving up on their multi-billion dollar industry which, in any event, digital ID will do nothing to hinder.

In addition, if they receive leave to remain, refugees and asylum seekers can secure a NIN for themselves and work here legally. So, all in all, the government’s argument for introducing digital ID is total codswallop.

It is obvious that tackling illegal migration has nothing to do with the UK governments alleged hope of foisting digital ID on us all. It is equally obvious that the restricting the right to work is not really the purpose of digital ID:

A new digital ID scheme will make it easier for people across the UK to use vital government services. The roll-out will in time make it easier to apply for government and private sector services, such as helping renters to quickly prove their identity to landlords, improving access to welfare and other benefits, and making it easier for parents to apply for free childcare.

So, “in time,” we will supposedly need digital ID to access services like child care, to receive “welfare and other benefits,” and to rent a home. But that’s not all. We will also need it to access “private sector services” such as those offered by banks. You’ll need your government approved digital ID to buy a home too, in time.

In short, a state issued digital ID gives the state total control over your life and, to a great extent, the economy.

Currently migrants given leave to stay, either permanently or temporarily, can use government issued biometric ID—digital identity that contains biological information—to “open a bank account.” Starmer’s biometric BritCard, and all digital ID, merely extends that government mandated “privilege” to the rest of us.

Starmer is a globalist member of numerous policy think tanks, including the Trilateral Commission. The policy to enforce digital ID on everyone has nothing to do with his government. That Policy emanated from globalist think tanks, like the Trilateral Commission, and was set by the United Nations as SDG 16.9 in 2016.

Starmer and the UK government are seemingly doing what they are told. But something doesn’t quite add up.

The global digital ID systems and networks that have been put into place, to date, do not require the issuance of any single biometric digital ID card or app. Rather, a smorgasbord of “vendor agnostic” digital ID products can be made “interoperable” and share data in a uniform machine readable format. If the SDG 16.9 plans for data interoperability proceed as envisaged, the data from your UK biometric digital ID driving licence—which you probably already possess—and your biometric digital ID passport, for instance, could be linked to all your purchases through your interoperable digital bank card.

The data from all these “vendor agnostic” digital ID products, because they each use interoperable machine readable data exchange formats, can then be hoovered up to the global digital ID database. At present, the World Bank’s ID4D looks like the most likely candidate. The UN’s World Bank has set the interoperability data standards that the digital ID database requires and has divided them into five categories:

Major standards to facilitate the technical quality and interoperability of the ID system related to: (1) biometrics, (2) cards, (3) 2D barcodes, (4) digital signatures, and (5) federation protocols.

For example, the Indian government’s Aadhaar unique digital ID card (or app) uses “the ISO/IEC 19794 Series and ISO/IEC 19785 for biometric data interchange formats.” These are approved World Bank ID4D interoperability standards. In this case, Indian’s biometric data can be exported in a “machine-readable format enabling ease of import into” the SDG 16.9 compliant global ID4D database.

In July 2022, the ID2020 Alliance—the group tasked with fulfilling SDG 16.9—appointed Clive Smith as its new executive director. Clive was the former Director of Global Operations at the United Nations Foundation Mobile Health Alliance. Speaking about his new role, Clive said:

ID2020 can play a pivotal role, helping ensure that the appropriately interoperable solutions – and related financial, legal, and regulatory guardrails – are in place, and become the foundation of digital ID in the decades ahead.

The interoperable digital infrastructure is the key to constructing our digital IDs from interlinked vendor agnostic digital ID products. In effect, our digital ID can be manufactured by the system, as we interact with it, without us having any one, designated digital ID app or card. That is the point of digital ID-linked product interoperability.

The UK government already has an SDG 16.9 compatible biometric digital ID platform called One Login. It is part of the Government Digital Service (GDS) and provides users with access to government services via their GOV.UK digital wallets. The system is hopelessly insecure and the risk of identity theft is high, but all digital ID systems are prone to criminal misuse, so there’s nothing unusual there.

In India R.S. Sharma, Chairman of the Telecom Regulatory Authority of India (TRAI), decided to demonstrate that claims of digital ID security flaws were all “conspiracy theories.” He published his Aadhaar number on, what was then, Twitter to prove the system was secure. Within hours, hackers had released his mobile number(s), personal Gmail and Yahoo addresses, his home address, date of birth, frequent flyer number, private photographs and bank account details to which—for a laugh but making their point—they sent some small payments.

Nevertheless, the interoperable digital ID infrastructure that is being installed globally means there are no technological reasons to account for the UK government’s attempt to introduce an extremely unpopular single, government issued digital ID. Especially seeing as it already has a digital ID system (One Login) that uses existing ID, such as driving licenses, to essentially achieve the same thing that the BritCard is supposed to deliver.

Compounding this unfathomable government strategy, the British have a long history of objecting to government issued ID. To expect us to go along with it this time is nonsensical.

Government issued ID was introduced in the First World War and abolished by public demand in 1919. They were reintroduced shortly after the start of the Second World War and withdrawn in 1952, again due to public opposition. The Blair Labour government tried again in 2010 and, though it was cost and election defeat, rather than unpopularity, that saw that attempt fail, government issued ID was widely opposed nonetheless. The government knows such national ID projects are extremely unpopular and it must have anticipated a political backlash.

Not only that, Starmer’s government decided to formally announce another government issued ID at a time when its popularity has never been lower. Notably, leading voices in the UK Reform Party have already taken a stance against the BritCard, as have those in the Conservative Party. Nor does the announcement do anything to assuage Labour’s alleged concerns about the so-called “far-right” as its supposed leaders have also come out against the BritCard move.

There is no realistic prospect that the government is going to get people to adopt its ridiculous BritCards. From Starmer’s and the Labour government’s perspective, this looks like political suicide. What’s going on?

After its initial leaky debacle, the contract for the cyber security for the government’s One Login was given to the US multinational Accenture led by Julie Sweet who sits on the Board of Trustees for both the World Economic Forum and the Center for Strategic & International Studies. Accenture is partnered with Peter Thiel’s Palantir and Thiel sits on the Steering Committee of the Bilderberg Group. Both Accenture and Palantir are strategic partners with Larry Elllison’s Oracle. Ellison, like Thiel, is currently highly influential within the US government. All three companies have close links to the intelligence agencies, but Palantir’s and Oracle’s are very close.

Palantir is deeply embedded within the UK government and its defence and health sector. Oracle is similarly central to the digital transformation of UK government and, as we have just discussed, so is Accenture. These US Tech giants, led by people close to the centre of global power, all want to see digital ID succeed in the UK and fully back UN SDG 16.9.

Ellison is known to be a close associate of former UK prime minister Tony Blair and reportedly the money-man behind the Tony Blair Institute (TBI). The TBI has been pushing for digital ID in the UK for years. But what is digital ID really about for think tanks and policy setting groups like the Trilateral Commission, the Bilderberg Group and the TBI?

It is all about using the harvested data to control our lives. Lest you have any doubt, in September 2024, Ellison told Oracle investors:

Citizens will be on their best behavior because we are constantly recording and reporting everything that’s going on.

In February this year, the TBI published a blueprint for what it calls the UK’s National Data Library (NDL). The TBI wants the data from all corners of the society and the economy, all public and private services, all industry, all business and all of us, to be stored in one unified central database: the NDL.

However, in order for the NDL to work, the TBI noted:

Harmonised personal identifiers, using a consistent number to refer to the same entity in different places, should be introduced to improve interoperability. [. . .] None of this would be possible without efforts to improve the broader data infrastructure, including efforts around interoperability and digital identity. [. . .] This allows the NDL to focus on closing a critical gap by addressing the legal, operational and structural barriers that prevent effective data use. Interoperability and even linkage efforts, welcome as they are, do not guarantee access or usability.

Clearly, the TBI is acutely aware of the interoperability that lies at the heart of the global digital transformation. The One Login GDS system is prepped for the completion of the necessary digital infrastructure. Digital ID is the linchpin that sets the entire system in motion. Therefore, it is essential to the government and its partners—Palantir, Accenture, and Oracle, etc.,—that we can somehow be cajoled into accepting digital ID.

Starmer’s BritCard is not intended to convince us to adopt digital ID. Its announcement is spectacularly ill-timed, the arguments offered to justify it are absurd and there is no reason to think the British public will ever buy in to it.

It is not unreasonable to speculate that BritCard is a bait-and-switch psyop.

The BritCard has stimulated debate about digital ID. I’m sure Newsnight and Question Time will cover it. We can argue the pros and cons and consider if we want digital ID. Then we will either accept or reject the BritCard, imagining that it is the totality of digital ID, and the issue will be resolved. Which I think is the point of BritCard.

The most likely outcome is that as anger is stoked and resentment swells, the completely unnecessary BritCard will be flung out along with the Labour government: again.

The door will then be open for the political saviours, be they the Tories, Reform or whomever, to come to power promising never to subject us to any more of these idiotic government issued ID schemes.

However, to keep pace with the digital revolution, our digital infrastructure, our cards and licenses, will need to be upgraded to facilitate the necessary interoperability.

Voila! We will rejoice in our victory and accept digital ID without even knowing it.

Source: https://iaindavis.substack.com/p/the-britcard-digital-id-psyop

Original Article: https://off-guardian.org/2025/10/07/the-britcard-digital-id-psyop/

UK Digital ID: The BritCard Bait and Switch

Iain Davis | substack.com/@iaindavis

In my previous article [above] I suggested that the UK’s proposed “mandatory” digital ID, called the BritCard, was a bait and switch psyop. I posited that the arguments presented by Keir Starmer’s purported Labour government, to supposedly justify the BritCard rollout, coupled with the timing of the announcement, the apparent inability to understand public opinion, and the lack of necessity for the BritCard, indicated that there was something amiss with the so-called government’s BritCard proposition.

It seems to me that the purpose of the BritCard gambit is to frame the Overton Window for the public debate about digital ID in the UK. People can accept or reject it, imagining the BritCard represents the totality of digital ID infrastructure. If the population rejects the BritCard they may well do so under the misapprehension they have defeated digital ID in the UK.

Subsequent developments have strengthened my view.

Digital ID is a global policy initiative that governments around the world, including the British government, are following, not leading. It is the United Nation’s (UN’s) Sustainable Development Goal (SDG) 16.9 which promises to “by 2030, provide legal identity for all, including birth registration.”

Even before the ink was officially dry on SDG 16.9, the ID2020 group, tasked with meeting the “identity” sustainability target, outlined what achieving SDG 16.9 would mean in practical terms:

[C]reate technology-driven public-private partnerships to achieve the United Nations 2030 Sustainable Development Goal of providing legal identity for everyone on the planet.

ID2020 further clarified the global policy objective:

By 2030, enabling access to digital identity for every person on the planet.

The objective of SDG 16.9 is to force not just approved “legal identity” but digital ID on every human being on earth. To this end, the UN has already created a nascent global digital ID database called ID4D. The ID4D Global Dataset aim to capture the data of “all people aged 0 and above.”

Run by the World Bank Group—a UN specialised agency—ID4D informs us:

The World Bank Group’s Identification for Development (ID4D) Initiative harnesses global and cross-sectoral knowledge, World Bank financing instruments, and partnerships to help countries realize the transformational potential of identification (ID) systems. [. . .] The aim is to enable all people to exercise their rights and access better services and economic opportunities in line with the Sustainable Development Goals.

At first reading this might not seem so bad. Therefore, it is very important to be clear about what it implies.

Your access to all “services” and all “economic opportunities” will be dependent upon you possessing the requisite digital ID; the entire economy—all services and all economic activity—must comply with “Sustainable Development Goals.” This means everything will be ordered by the global governance system, not by national governments. Finally, “partnership” means public-private partnerships.

If you think I may have put an unwarranted pejorative spin on the ID4D statement consider that the UN’s SDG 16.9 makes no mention of “digital ID,” only “legal identity.” Yet, ID2020, the UN’s own body responsible for implementing SDG 16.9, had already committed to the global rollout of digital ID before the UN officially announced its global governance ID agenda.

The UN “regime” is not an honourable or trustworthy organisation and we must interpret its goals and public statements carefully to understand the actual implications. With far less fanfare, and allowing for a suitable cooling-off period, in 2023, the UN finally came out of the closet and simply said it wanted “Digital IDs linked with bank or mobile money accounts.”

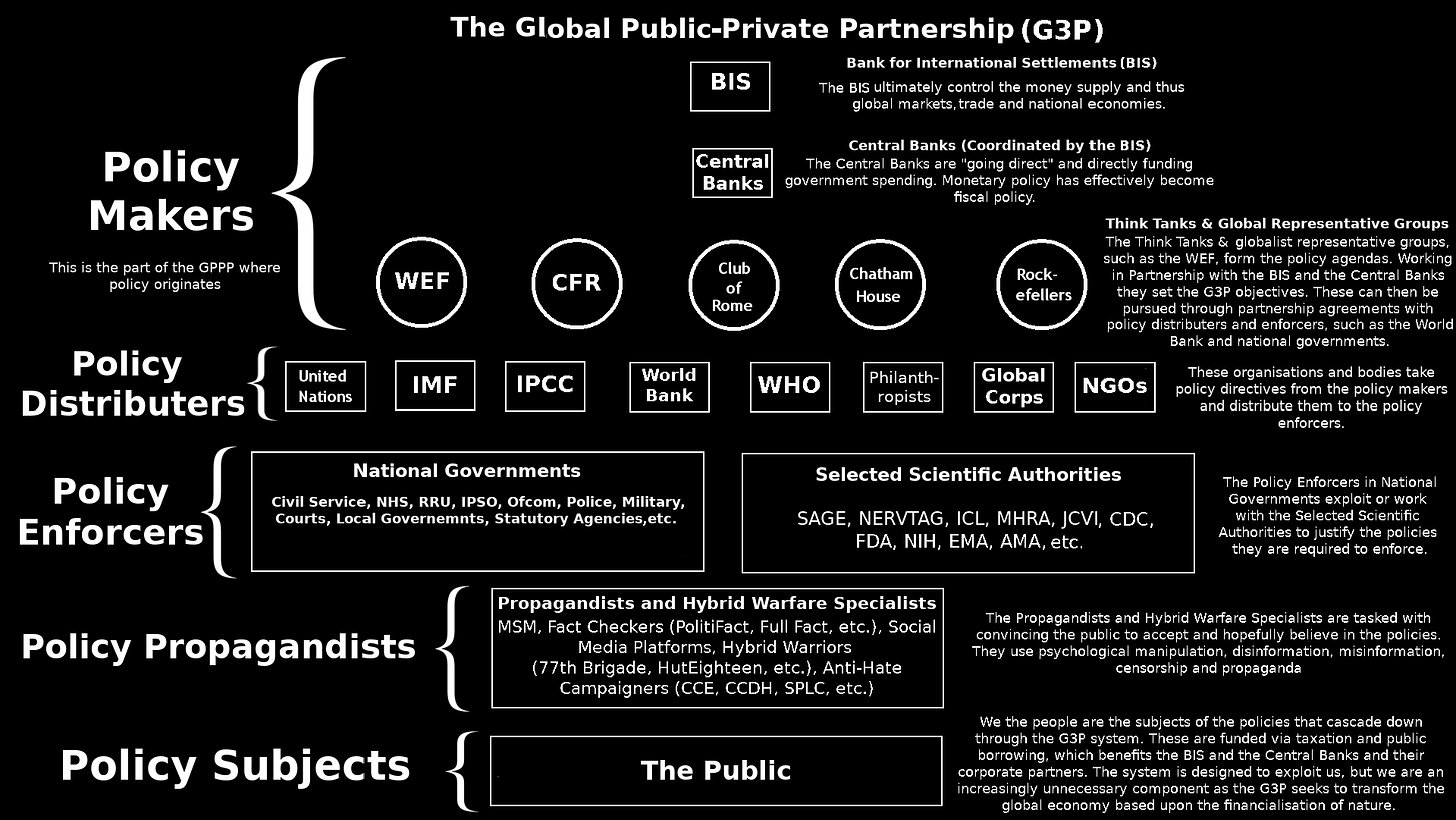

The global public-private partnership (G3P)—essentially a nexus between central banks, international policy think tanks, the UN, multinational corporations, NGO’s and other “philanthropic” organisations, and governments—is propelling the global rollout of digital ID. ID4D “partners” include the Gates Foundation, the Omidyar Network, and the World Economic Forum (WEF) that represents “leading global companies” seeking to “shape the future.”

Leading WEF Partners include US data and AI giant Palantir. The WEF runs a number of global research “Centres” and Palantir is a key partner in five of them including the Centres for Cybersecurity and for the Fourth Industrial Revolution.

The UN began as a public-private partnership. In 1998, having undergone a “quiet revolution,” it formally shifted away from being an intergovernmental organisation to become a public-private global governance regime that promotes “business-friendly legislation.”

Like the UN ID4D project, the central bank of central banks—the Bank for International Settlements (BIS)—envisages a “unified ledger” that will oversee every transaction on earth. The power to control all commerce extends to all business to business (B2B) transactions. The Bank of England and the Federal Reserve Bank of New York are among the central banks working on the associated BIS-led Project Agora :

The project aims to test the desirability, feasibility and viability of a multi-currency unified ledger for wholesale cross-border payments. [. . .] The project is a public-private collaboration that seeks to use new technology to improve the correspondent banking model.

To appreciate what this new global monetary system is designed to achieve we need to understand “tokenization.” McKinsey explains:

Tokenization is the process of creating a digital representation of a real thing. [. . .] [T]okenization is a digitization process to make assets more accessible, [. . .] tokenization is used for cybersecurity and to obfuscate the identity of the payment itself, essentially to prevent fraud. [. . .] [T]okenized financial assets are moving from pilot to at-scale development. McKinsey analysis indicates that tokenized market capitalization could reach around $2 trillion by 2030 (excluding cryptocurrencies like Bitcoin and stablecoins like Tether). [. . .] Larry Fink, the chairman and CEO of BlackRock, said in January 2024: “We believe the next step going forward will be the tokenization of financial assets, and that means every stock, every bond … will be on one general ledger.”

The BIS has been planning to seize the opportunity presented by tokenisation operating on a “one general” or a unified ledger for some time:

A new type of financial market infrastructure – a unified ledger – could capture the full benefits of tokenisation by combining central bank money, tokenised deposits and tokenised assets on a programmable platform

Digital ID is inextricably linked to “onboarding”—accessing and using—programmable digital currencies (PDCs) such as stablecoins and central bank digital currency (CBDC). The push to get us to adopt programmable digital currency is also a public-private global project. The BIS spells out why digital ID is a prerequisite for using programmable digital currency:

Identification at some level is [. . .] central in the design of CBDCs. This calls for a CBDC that is account-based and ultimately tied to a digital identity. [. . .] A digital identity scheme, which could combine information from a variety of sources [. . .] will thus play an important role in such an account based design. By drawing on information from national registries and from other public and private sources, such as education certificates, tax and benefits records, property registries etc, a digital ID serves to establish individual identities online. [. . .] [S]ystems in which the private and official sector develop a common governance framework and strive for interoperability between their services, [. . .] represent the furthest-reaching model. These allow administrative databases to be linked up, further enhancing the functionality and usefulness of digital ID.

The BIS is quite clear about the interoperable model that will “allow administrative databases to be linked up.” In such a model your biometric—biological identifier—digital ID (e-ID) will be constructed by your use of the “interoperable” system framework.

Your e-ID will provide both public and private organisations access to your data. For example, as long as they have the required access permission, approved private finance “partners” can check your identity attributes, such as your qualifications, tax records, history of any welfare payments you may have received, and assess the value of any of your other e-ID attributes, such as property or other assets you might own. This can help them decide if they will offer you credit, how much interest to charge you, whether to offer you insurance or not, and at what price, etc.

In addition, every time you make a transaction with your PDC—by virtue of it being directly connected to your e-ID—public and private parties with sufficient access permissions to the application programmable interface (API) layer will be able to use your e-ID attributes to make decisions about processing payments, in real time, such as allowing or disallowing your transactions.

The BIS illuminates:

APIs ensure the secure exchange of data and instructions between parties in digital interactions. [. . .] Crucially, APIs can be set up to transmit only data relevant to a specific transaction. [. . .] An example is “open banking”, which allows third-party financial service providers to access transaction and other financial data from traditional financial institutions through APIs. For example, a fintech [Financial Technology company] could use banks’ transaction data to assess credit risk and offer a loan at lower, more transparent rates than those offered by traditional financial institutions. [. . .] Payment APIs may offer software that allows organisations to create interoperable digital payment services to connect customers, merchants, banks and other financial providers. [. . .] [T]he recipient’s bank (or financial services provider) needs to agree to the transaction on the customer’s behalf. During this [. . .] step, it is verified that the transaction satisfies rules and regulations. [. . .] Once there is agreement, in [the next] step funds are transferred and made available to the recipient immediately.

Such a system could, and it may offer all kinds of cost savings and other benefits. But behavioural and, ultimately, social and economic control, is what the likes of the UN, the BIS, and their partners desire. Speaking in October 2020, BIS General Manager Agustín Carstens explained why PDCs are nothing like any form of money we are currently familiar with:

The key difference with the CBDC is the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability, and also we will have the technology to enforce that.

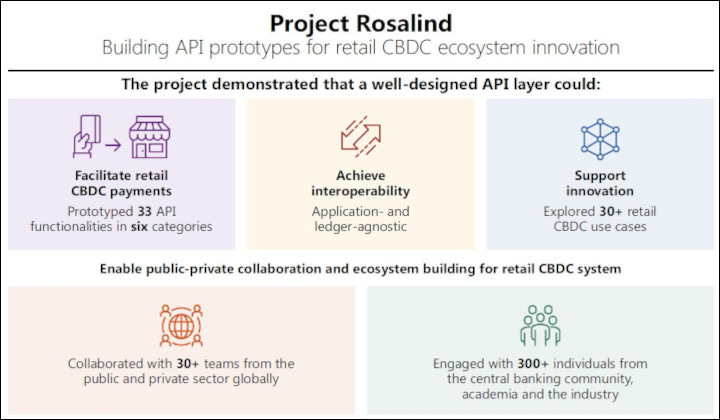

Again, “interoperability,” enabling universally recognised e-ID to be assigned to all transactions, using internationally accepted PDCs, allows API’s to precisely control any transaction, anywhere, between any parties, by using digital agreements, often called “smart contracts.” The BIS collaborated on Operation Rosalind with the Bank of England to develop the smart contract functionality we will all be subjected to in the UK once we accept e-ID and, as planned, PDCs.

Distributed Ledger Technology (DLT)—most likely blockchain—will record, oversee and control all digital transactions on a “unified ledger.” The Operation Rosalind social engineers concluded:

Ledger API layer: This layer translated smart contracts into API calls and transformed API requests into a format understood by, and actionable for, the central bank ledger. [. . .] This could support many use cases, such as third-party payment initiation, external smart contract applications and budgeting applications.

Smart contracts on the API layer could be used to automatically initiate “third party payment” such as taking taxes, fines, private penalty charges, utility payments, and so on, directly from your “digital wallet.” Using smart contracts, your e-ID assigned PDC can be programmed, in real time, to control what you buy, from whom, where and when.

Bo Li, the former Deputy Governor of the People’s Bank of China, and the current Deputy Managing Director of the International Monetary Fund (IMF), speaking at the Central Bank Digital Currencies for Financial Inclusion: Risks and Rewards symposium, explained the power that programmable digital currency provides to those with the approved ledger permissions:

CBDC can allow government agencies and private sector players to program [CBDC] to create smart-contracts, to allow targeted policy functions. For example[,] welfare payments [. . .], consumption coupons, [. . .] food stamps. By programming, CBDC money can be precisely targeted [to] what kind of [things] people can own, and what kind of use [for which] this money can be utilised. For example, [. . .] for food.

Whatever falsehoods the government or the media might tell you about digital ID, the fact is digital ID is a global governance policy initiative and the objective is to control our behavior and our lives. Digital ID (e-ID) is the keystone for a global system of oppression and once we have accepted e-ID the rollout of a global network of programmable digital currencies (PDCs) will immediately follow.

Whether we accept BritCard or not, the UK government has already adopted what the BIS called “the furthest reaching model” of e-ID. The system is managed by the UK government’s Office for Digital Identity Attributes. The “Office” has registered the current slew of private companies that have won bids to provide “digital ID and attribute services” to all of us in the UK. Notable e-ID and attribute service providers include Deloitte (Go Verify) and Mastercard.

In order to become a “trustworthy digital verification service (DVS),” global corporations like Deloitte and Mastercard must adhere to the UK Digital Identity and Attributes Trust Framework. The framework sets the “technical and operating standards for use across the UK’s economy [that] will help to enable international and domestic interoperability.” International interoperability will ensure all the data harvested from the UK population is available to the architects of global governance. Possibly via the ID4D or the BIS unified ledger, for example.

In order to ensure both domestic and international interoperability between all e-ID products and services, the DVS-provider must use the approved “data schema.” Section 14 of the framework provides all the technical information-exchange standards that will enable interoperability.

The interoperability standards allow all the data harvested from you to be stored and transmitted “in a machine-readable format” that is “interoperable with other certified services and relying parties” both “in the UK and internationally.” This means, for instance, that data seized from your use of your digital biometric driving licence, or passport, can be connected to the separate “trustworthy” DVS provided by, for example, the issuer of your bank card.

This interoperable system means that a single, government issued BritCard is completely unnecessary and achieves nothing whatsoever. The e-ID framework that the government has been developing for years, and already has in place, does not need and does not benefit from BritCard.

Yet, when more than 2.8 million people apparently signed a government petition opposing Britcard, in response, the government said:

We will introduce a digital ID within this Parliament. [. . .] [T]he new digital ID will build on GOV.UK One Login and the GOV.UK Wallet to drive the transformation of public services. Over time, this system will allow people to access government services – such as benefits or tax records – without needing to remember multiple logins or provide physical documents.

Beyond the demonstrable reality that the government doesn’t care what we think, this statement is gibberish. The GOV.UK One Login system was designed around the interoperable UK Digital Identity and Attributes Trust Framework. Farcically, One Login’s hopeless cybersecurity failings led the government to revoke the “framework” accreditation for its own service in May of this year. The government then handed multi-million pound contracts to PA Consulting and the US Tech Giant Accenture to try and fix all the One Login problems and hopefully regain its own interoperable framework accreditation.

BritCard is not framework compliant and is not listed as a DVS-provider. The BritCard concept has not been put out for either market or public consultation. BritCard does not exist in any meaningful sense and is nothing but a PR stunt. The only question is what is the purpose of the stunt. There are some telling clues.

Palantir is a “data-mining juggernaut” that works closely with US intelligence and national security agencies. It is a UK strategic defence partner, and operates the UK NHS Federated Data Platform which “connects vital health information across the NHS.”

Palantir also operates a number of its own strategic partnerships with other global corporations. For example, its partnership with KPMG affords KPMG access to “Palantir Foundry”—Palantir’s AI software platform. The government then awarded KPMG the contract to promote and rollout Palantir’s NHS Federated Data Platform across the country. This is understandable because Palantir Foundry is also the AI software platform digitally transforming the UK government.

Palantir’s partnership with the UK digital verification service (DVS) provider Deloitte enables both companies to “break down institutional barriers, organize fragmented data, and transform information into decisive action.” It’s partnership with Accenture will supposedly deliver “transformational outcomes,” and it partnership with fellow US intelligence cut-out Oracle will “accelerate AI” for businesses and governments. This is why the UK government has given Oracle the contract to do just that.

With its vast array of networked connections into the heart of the British state, it is no surprise that the UK government is heavily reliant on Palantir Gotham to plan missions and run investigations “using disparate data.” This will enable state operatives—or Palantir operatives, depending on how you look at it—to “produce actionable intelligence based on the full ecosystem of available data.” For Palantir, that “available data” in the UK appears to be pretty much all of it.

In the UK, Gotham is fully “interoperable with any legacy system,” quickly makes “connections across massive scale, dispersed datasets,” and enables the sharing of “investigative reports” either “internally” or with “partner agencies,” who ever they may be. If it existed, BritCard would add nothing other than additional hassle.

Once again, interoperability, is the key to hoovering up data from all “dispersed datasets” and Palantir is among the North American, UK, and European global technology firms to have already invested in the interoperable digital attributes framework in the UK. Louis Mosley, Executive Vice President (EVP) of the UK and Europe for Palantir Technologies, told the House of Commons Science, Innovation and Technology Committee—which was deliberating on the UK governments e-ID plans:

Interoperability is our [Palantir’s] bread and butter. As the Chair described, one of the core value-adds of the software is the fact that it can interact with and read and write data from pretty much every system out there. [. . .] [W]e provide an enormous amount of control and governance to the organisations that use our software.

With this mouthwatering and unprecedented control and governance on the near horizon, what on earth possessed the government to seemingly throw the whole thing into jeopardy by trying to stamp digital ID onto a very resistant British population? When it came to office a little over a year ago, Labour categorically rejected digital ID. Then Home Secretary Yvette Cooper said: “It’s not in our manifesto. That’s not not our approach.” What’s changed? Has Starmer’s government lost its collective mind?

Or is there a more plausible explanation?

In a very revealing interview with former BBC political editor John Pienaar for Times Radio, Louis Mosley made a series of claims regarding why Palantir had decided—and very publicly announced—it will not back BritCard. Bizarrely, Mosley said he had “personal concerns about digital ID.” He added that Palantir will “help democratically elected governments implement the policies they have been elected to deliver.” He noted, however, that digital ID was not in Labour’s election manifesto and that the decision to adopt digital should be taken at “the ballot box.” Therefore, he demurred, the BritCard project “isn’t one for” Palantir.

Of course, harvesting every possible scrap of data to enable “control” of the population wasn’t in the Labour Party’s manifesto either, but that hasn’t stopped Palantir from enthusiastically diving into that project. As for Mosley’s personal qualms about such things, if he holds them, he is definitely working for the wrong intelligence-linked “data-mining juggernaut.”

It was Pienaar who perhaps made the most interesting comment of all:

Among the other views, privately expressed by ministers, about the digital ID, a program, which at least one senior politician, who thought this wasn’t going to happen, it was just be too difficult. Do you think it’s gonna happen?

Pienaar is a member of the Establishment. He is privy to the the off-the-record discussions of ministers. His observation is worth thinking about.

Mosely replied:

One of my concerns about it is the technical feasibility of it or, maybe better expressed, the technical necessity of it. No doubt, we have all had the experience of engaging with parts of government where the online experience leaves something to be desired. It needs improvement.

However, we are in a world now where, I think, there are at least a dozen unique identifiers for each of us in government. We have passports, we have driving licenses, we have unique tax codes, we have national insurance numbers. Now, each of these sits in a silo and doesn’t talk to the other, isn’t harmonised. There’s no way for government to easily jump from one to another.

That could be achieved, in the back-end, with relatively little effort and I think that would go a long way to improving that citizen experience. I don’t see the need for an additional form of identification on top of the many that already exist.

Over the last decade or so, ably assisted by mega-corporations like Palantir, Deloitte, and Oracle, successive British governments have been putting the interoperable digital ID infrastructure together. Mosley casually refers to this as the “back-end.”

Our adoption of digital ID is absolutely essential to the state’s, and its private partners’, long-term plans. At some point, we have to be convinced to use it.

Let’s assume Pienaar is right: the government knows we will not accept e-ID. How, then, does it coerce us into adopting it?

It announces a Mickey Mouse, pretend digital ID and deliberately raises the specter of government overreach in our lives. It knows we will react viscerally and anticipates the backlash. In so doing, it focuses the public debate on the introduction of a single, government issued e-ID which it doesn’t need and has put no effort into developing. Waiting for us is the real digital ID system that government and its corporate partners, like Palantir, have actually been engineering.

Along comes the saviour, in this instance embodied by Palantir and Louis Mosley, pointing out to us that we don’t need BritCard. We just need to improve the “back-end” of the governments system so that all our cards and licenses can “talk to the other” in harmony. And that is the essence of genuine digital ID.

It seems highly likely that we will reject BritCard. An ignominious defeat will be heaped on the government and talked about incessantly by the media as it extols how we Brits will never succumb to digital ID.

It’s just that we need to tweak the “back-end” a bit to improve our “citizen experience” as we interact with the online public-private state.

BritCard is a bait and switch psyop. Don’t fall for it.

Source: https://iaindavis.substack.com/p/uk-digital-id-the-britcard-bait-and

Related:

Comments ()