The Tokenized Economy Is Here | Global Financial System Is Undergoing A 'Structural Reallocation'

IBM Says 'The Tokenized Economy Is Here.' Tokenized Real Estate And Fractional Ownership Go Mainstream, As The IMF Says Global Financial System Is Undergoing A 'Structural Reallocation'

The WinePress News | The WinePress | thewinepress.substack.com

2026 is already proving to be a very pivotal year for tokenization as the world quietly races to implement domestic and international AI controlled grids, and trackable and traceable blockchain ledgers that store ownership rights of everything. While tokenization is slowly starting to get some occasional mainstream press attention, for the most part this radical transformation of the global financial system is still being constructed in the shadows while the masses are distracted elsewhere.

Computing giant IBM earlier this year put out its 2026 Global Outlook for Banking and Financial Markets report1, which focused specifically on tokenization and how banks will need to adapt to this new paradigm.

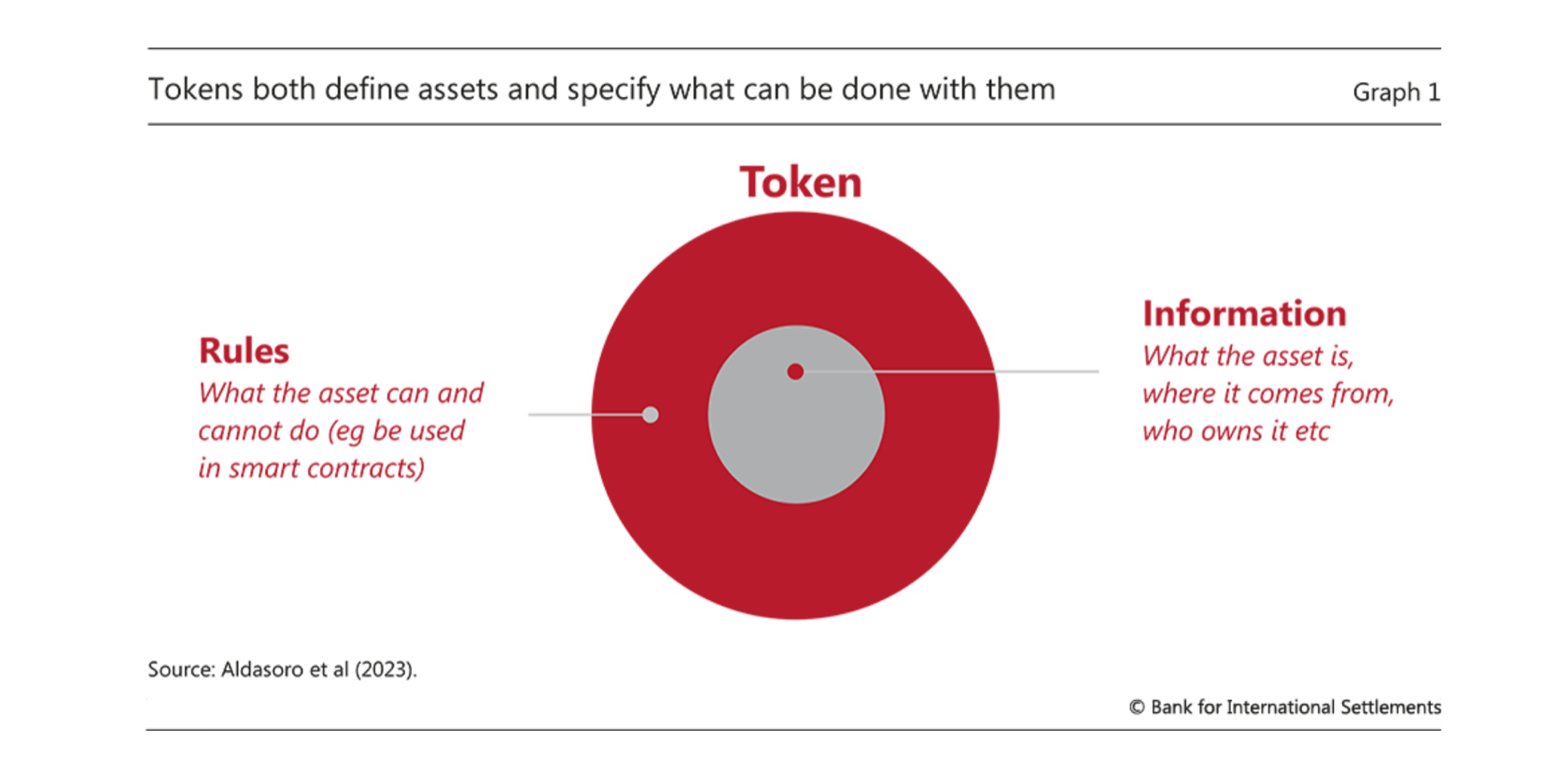

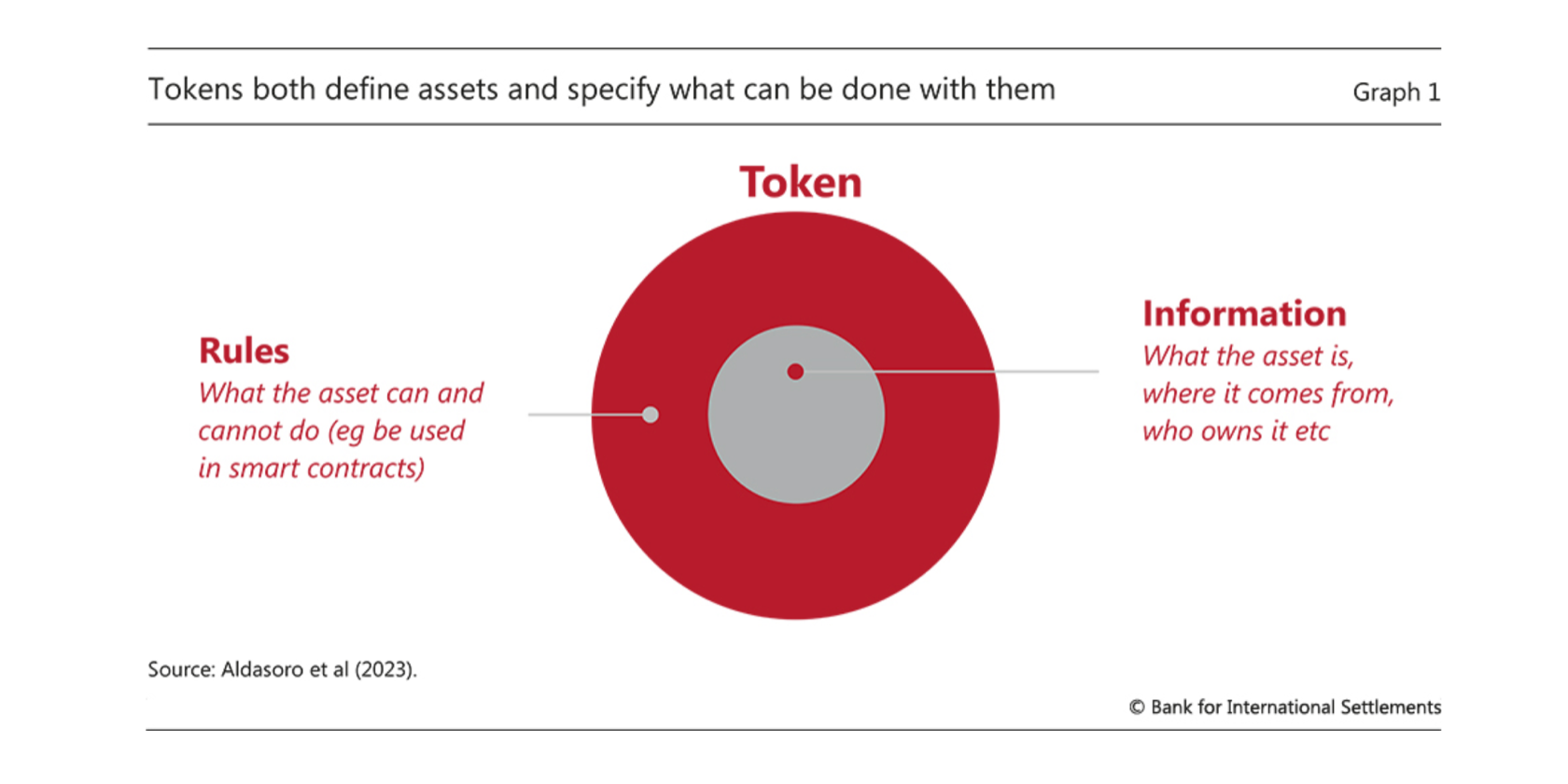

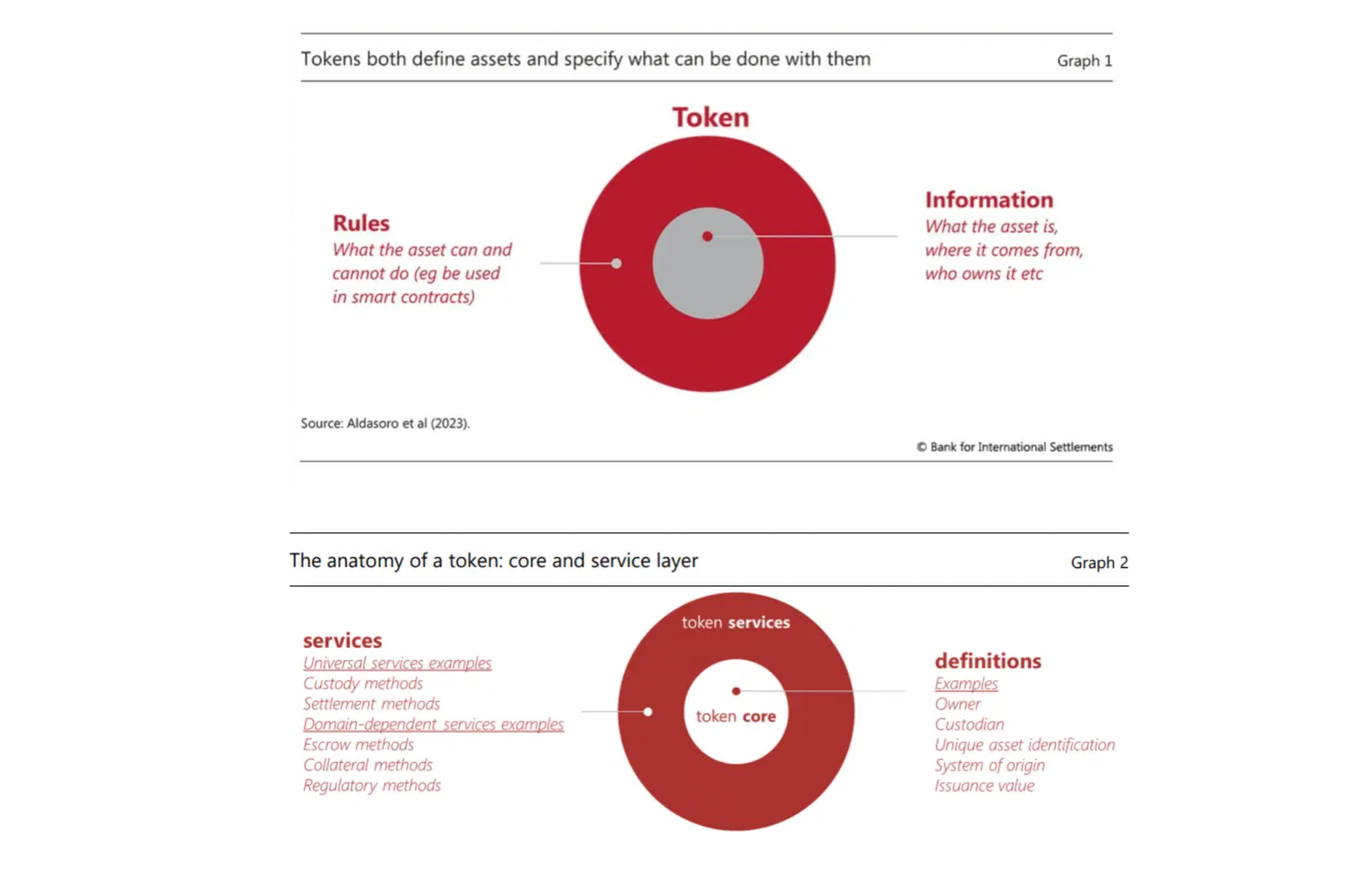

Again, as a reminder: a “token,” as defined by the Bank for International Settlements (BIS)2 - nicknamed the “central bank of central banks” - “are entries in a database that are recorded digitally and that can contain information and functionality within the token themselves. Digital tokens can represent financial or real assets.” A token collects information3 about that underlying digital money or asset: ownership, dates of purchase/sale, transaction dates, and so forth.

IBM says, “Tokenization enables the instantaneous transfer of assets and value anywhere, including across borders, at any time and at a fraction of traditional costs.” The group adds:

“The on-chain economy—which turns real-world assets into digital tokens that can move instantly on blockchains—is arriving faster than most expected. It’s poised to reshape financial services, with architectures, market access, and product pricing all in play. Already, major neobanks have captured market share in the off-chain digital economy while fintech players dominate foundational layers of the on-chain economy.

“At its core, tokenization transforms ownership rights in financial, monetary, or physical assets into digital tokens on a distributed ledger. Transformation will extend well beyond payments and lending. The impact is structural: it enables fractional ownership and instant transfers of securities across digital wallets, while simultaneously reducing costs and boosting liquidity.”

“Fractional Ownership” is a big component of tokenization, something I’ve highlighted before; a concept that BlackRock CEO and World Economic Forum co-chair Larry Fink has described as allowing an item to be split into multiple tokens representing partial ownership and contractual rights.

Fractional ownership is especially present in large-ticket and expensive items, particularly housing and real estate, for example. I have previously warned that in order to unlock the housing market in the United States and other Western nations, real estate would have to be tokenized and fractionally broken-up into smaller tokenized contracts.

Last month, Fannie Mae partnered with Coinbase, one of the largest crypto and token exchanges in the world, to allow crypto and stablecoin payments4 for home loans and mortgages, opening the doorway for fractional ownership — which is a nice way of saying renting but never owning.

This concept is beginning to enter the mainstream. This month, Business Insider5 published a detailed article titled “The new American dream: owning just part of a home.” The paper lists one company called Jubilee that provides “fractional ownership” of real estate which, in their case, works like this:

Say you find a house you want to buy, but you can’t afford the down payment, or you want lower monthly costs. You and Jubilee make a combined offer on the house — Jubilee purchases the land with cash, and you pay for the structure with a separate mortgage. Slicing up the purchase this way makes it vastly cheaper for you than buying the whole thing. Jubilee then offers you a 99-year lease on the land, for which you’ll pay monthly rent in addition to your mortgage. The total monthly costs are lower or roughly comparable to a traditional purchase, the company says, and the required down payment shrinks dramatically.

You can buy the land from Jubilee at any point for an amount determined by a third-party appraiser. Or, if you want to sell down the line, you can package the home and land together again, and Jubilee will get a cut of the total sales price. If the land accounted for 65% of the initial purchase price, the company will get 65% of the proceeds when it sells.

While tokenization was never explicitly mentioned in the article, the concept is still there and tokenization will absolutely be used for housing, vehicles, and many other expensive purchases, which IBM and BlackRock have said would happen.

Furthermore, IBM explains how “AI and tokenization should not be viewed as separate technological advancements. When thoughtfully designed and implemented, they can

reinforce one another.” Because of this, IBM references how the pair will advance the 4th Industrial Revolution, a term coined by WEF founder Klaus Schwab to describe the augmented and interconnected world we are moving into.

“Perhaps more exciting is the intersection of AI and tokenization. As corporations redesign processes for AI-driven automation, AI agents will increasingly rely on tokenization to autonomously interact with supply chains—refilling stock, executing orders, paying invoices—all through programmable features. By financially enabling robotics, financial services can become a pillar of the Fourth Industrial Revolution.”

Ultimately, according to IBM, they “expect 2026 to be a turning point for tokenization.”

{kind=link}

IBM warns banks and financial institutions of a Kodak Moment of sorts: either with the times now or get left in the past, because the world is tokenizing, like it or not.

“By 2030, tokenized assets, stablecoins, and central bank digital currencies (CBDCs) won’t be experimental. They’ll be table stakes. The institutions that thrive will be the ones that made hard decisions in 2026 and 2027: decisions about new value streams, business opportunities and risks, core banking systems, modernized computing platforms and hybrid cloud infrastructure, ecosystem roles, governance, and talent. The ones that hesitate will likely find themselves outpaced—not just by fintechs, but by corporate and institutional clients who will quietly move their capital, trust, and business to platforms built for a tokenized world.

“The tokenized economy won’t wait for stragglers. Neobanks are already forging ahead with deeply integrated, token-native architectures that give them a commanding edge. They embed cryptocurrencies and stablecoins as core elements of their platforms, not mere add-ons. Banks that build token-ready cores, secure ecosystem partnerships, and deploy custody infrastructure now will be able to capture the high-margin opportunities in 2030. Those still modernizing legacy cores will be playing catch-up in a market that’s already moved on.”

The International Monetary Fund (IMF) recently echoed a similar sentiment as well in regard to tokenization.

Tobias Adrian, Financial Counsellor and Director of the Monetary and Capital Markets Department at the IMF, and former Senior Vice President of the Federal Reserve Bank of New York, published a note6 this month simply called “Tokenized Finance,” who articulated that tokenization isn’t simply just an upgrade but an entire replumbing of the global financial system.

He begins his dissertation by stating that “the global financial system is undergoing a transition that is often described as technological but is fundamentally institutional,” and says “tokenization constitutes a structural reallocation of trust within the financial system.”

One thing he is careful to note is that as different nations take various setups — whether it’s going the more privatized route with stablecoins, or the stringent public route with central bank digital currencies, or somewhere in the middle with a hybrid format — many of them should and will be interoperable, meaning the different tokenized frameworks will be able to work together for cross-border trade, but will require international frameworks.

“The tokenized ecosystem is likely to remain pluralistic, with multiple platforms operated by different consortia, infrastructures, and jurisdictions. In such an environment, interoperability becomes not only a technical concern but also a monetary and financial stability issue. If settlement assets, liquidity pools, or collateral frameworks differ across platforms, fragmentation could impair par convertibility, reduce netting efficiency, and complicate crisis management. Without common standards, liquidity could fragment across platforms, undermining efficiency and increasing risk.”

However, and more controversially, Adrian reveals that since everything becomes code on a blockchain, that code can then be manually over-ridden and rewritten, and will require much greater control and ID verification.

“Therefore, the governance challenges concern not only code quality but also the processes that design, validate, modify, and, if necessary, override code.”

“Algorithmic risk differs from traditional operational risk in important aspects. Errors can propagate instantaneously and autonomously, without human intervention. A faulty price feed or coding error can rapidly trigger cascading liquidations before authorities respond. The very features that make smart contracts efficient—speed, determinism, and automation—can also amplify the consequences of design flaws or data errors.

“Therefore, effective governance requires multiple layers of control. Formal verification and independent audits should be mandatory for systemically important contracts. Change management processes must be transparent and subject to regulatory approval. Crucially, tokenized systems should incorporate clearly defined ex-ante intervention mechanisms in governance frameworks that allow contract execution to be paused or adjusted under predefined emergency conditions.

“Tokenization embeds governance in code, which could be referred to as “code is law.””

And this right here is another huge reason tokenization is so dangerous. If you don’t hold it, you don’t own it; and fractional ownership is no ownership at all. This goes beyond just some poorly written code and “hallucinogenic” AI. Once ownership has been surrendered to central banks and third-party custodians and the government, then these entities can manipulate people’s digital assets, social credit scores associated with digital IDs, and more. This is why I warned7 in the last edition of RTT that tokenization is also a war on paper money, contracts and information, just like we similarly read about in the dystopian novel Fahrenheit 451.

This process aligns with what the World Economic Forum (WEF) wrote in a post8 in 2024 titled, “’Code as Law’: The tokenization of financial assets and the paradox of programmability.”

The WEF is very much pro-tokenization, and in its post wrote, “In short, the real benefits of tokenization may not be reaped, unless the blockchain ledgers on which it rides are open, permissionless and support programmability.” They go on to describe the concept of “code as law” in these blockchains, and recommend mitigating Know-Your-Customer (KYC) and Anti-Money Laundering (AML) activity rather than nerfing the technology itself.

“At its core, programmability transforms code into enforceable legal contracts or specific market functions when interacting with tokenized asset values. This “code as law” characteristic inherently constrains intermediaries’ discretionary choices. While this constraint helps reduce moral hazard in financial institutions systemically, it also means individual intermediaries will face increasing commoditization. With limited discretion over asset composition and other operational choices, institutions will find it harder to differentiate themselves, likely leading to an erosion of traditional market power as their functions become increasingly automated.

“This transformation points to a broader shift in financial markets. Tokenization is poised to increase liquidity in previously illiquid assets while simplifying the balance sheet structure of financial institutions in terms of asset composition.

“The result will be a movement away from traditional balance-sheet-heavy intermediation in credit and payment activities toward more market-based price discovery and risk sharing, fundamentally changing how risks and capital are allocated across the economy. As tokenization gains momentum, regulators would do well in regulating the activity and not the technology.”

Proverbs 22:7 The rich ruleth over the poor, and the borrower is servant to the lender.

This is why the WEF says “You’ll Own Nothing And Be Happy” because they and other globalists want to force nations into tokenized slavery, ruled and governed by lines of code that can crash, glitch, or be manually over-written at someone’s discretion. This is all the more reason we must warn others and resist this system by decentralizing and going analogue as much as we possibly can.

Original Article: https://thewinepress.substack.com/p/ibm-says-the-tokenized-economy-is

Comments ()