Tokenization Of Real-World Assets Is A Tool Of Conquest, Not Liberation

Patrick Wood | technocracy.news

The promoters of real-world asset tokenization use the language of liberation. Democratization. Financial inclusion. Access for all. Frictionless ownership. These are the words of a sales pitch.

The documents tell a different story.

When you strip away the marketing and read the legal frameworks, the regulatory architecture, the institutional white papers, and the published visions of the men building this system, a single conclusion emerges with prosecutorial clarity: tokenization is not a new form of ownership. It is a new form of conquest. And the conquered will not know what happened to them until the system is complete.

This article presents the verdict. The evidence is already in the record.

I. The Word They Chose: Usufruct

Start with the language. Not the promotional language, but the legal language.

The late Dr. Michael S. Coffman, a good friend of this editor, spent decades investigating the legal frameworks embedded in United Nations environmental and land governance documents. What he found was not subtle. The UN’s own legal drafters had chosen a specific term to describe the relationship between individuals and land under their proposed governance frameworks. The term was usufruct.

Coffman did not invent this framework and impose it on UN documents. He found it inside them. Then he investigated what the word actually meant.

His conclusion, published in 2014, was precise:[1]

“By definition, usufructuary rights are the rights to use and enjoy the profits and advantages of something belonging to another, as long as the property is not damaged or altered in any way. Conceptually, it is similar to renting or leasing something within limits set by its true owner. The usufruct system of property use is derived from the Latin word ususfructus. Originally it defined Roman property interests between a master and his slave held under a usus fructus bond. The Romans expanded this concept to create an estate of uses in land rather than an estate of possession. Having seized lands belonging to conquered kingdoms, the Romans considered them public lands, and rented [ususfructus] them to Roman soldiers. Thus the emperor retained the estate [possession] in the lands, but gave the occupier an estate of uses.”

Read that definition again. The estate of possession — title, ultimate control, the right to revoke — remains with the sovereign. The occupier receives an estate of uses — the right to work the land, collect its fruit, and pay tribute — for as long as the sovereign permits.

This is not a metaphor for what tokenization does. This is the precise legal architecture of every major institutional real-world asset tokenization platform operating today.

The UN chose this word deliberately. Their legal drafters are among the most sophisticated in the world. When they write usufruct into a convention, they know exactly what they are invoking: a two-thousand-year-old conquest administration tool, first deployed by an empire that needed to incentivize soldiers to occupy foreign territory without surrendering imperial control over it.

Coffman saw Stage One of this system clearly: regulatory usufruct applied to American land through environmental and biodiversity frameworks. He did not live to see Stage Three. But he handed us the vocabulary.

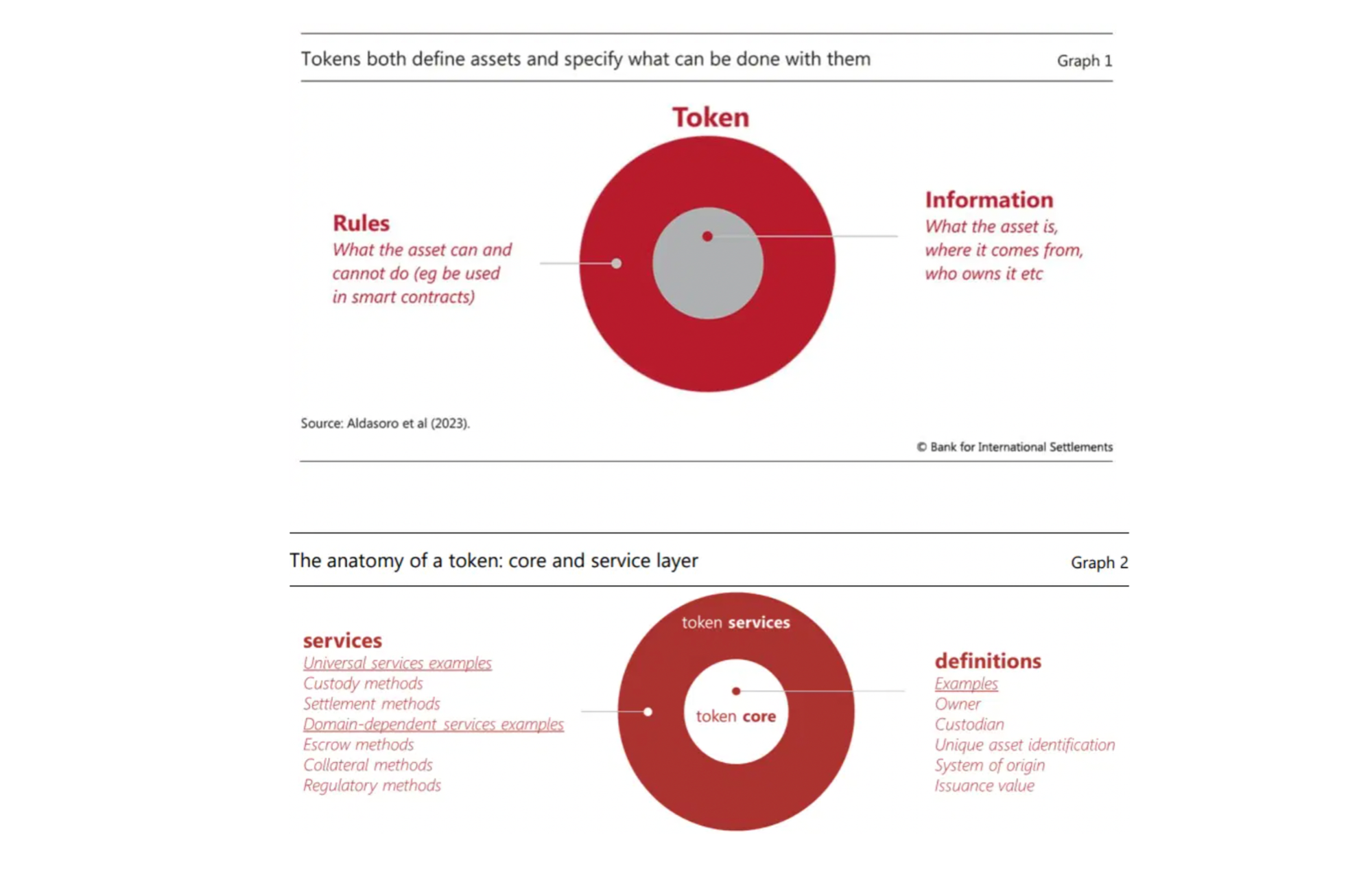

II. The Digital Usufruct

Real-world asset (RWA) tokenization is the conversion of physical assets into digital tokens on a blockchain. Proponents describe it as a revolution in ownership. Larry Fink of BlackRock calls it “the next generation for markets, the next generation for securities.”[2] In his 2025 Annual Chairman’s Letter, he stated it plainly: “Every stock, every bond, every fund, every asset can be tokenized.”[3]

Examine the architecture of what BlackRock has actually built.

BlackRock’s BUIDL fund is a tokenized money market fund built on the Ethereum blockchain. It is permissioned, meaning access requires identity verification. Token transfers are restricted to whitelisted counterparties. The underlying assets are held in institutional custody. The smart contract governing the tokens includes freeze functions and forced redemption capabilities controlled by BlackRock as administrator.[4]

The token holder does not hold the underlying asset. He holds a yield-bearing instrument representing a beneficial interest in an institutionally managed pool. He receives the income stream. He does not hold title.

This is Coffman’s Roman framework, digitized.

The token holder is the frontier soldier. He believes he is a settler. He is a usufructuary. He receives the fruit of the land. The emperor holds the land.

Franklin Templeton’s BENJI fund operates on the same architecture. Securitize — the dominant tokenization platform serving BlackRock, Hamilton Lane, and KKR — enforces transfer restrictions, freeze functions, and forced redemption capabilities at the contract level.[5] Ondo Finance delivers tokenized treasury yields to retail participants without custody of the underlying securities.

Every major platform has a freeze function. Every major platform requires identity verification. Every major platform places the underlying asset in institutional custody. This is not incidental. It is the architecture.

The estate of possession remains with the institution. The token holder receives an estate of uses.

The vocabulary has changed. The property structure has not.

III. Programmability Is the Weapon

Traditional property is dumb. A deed does nothing on its own. It cannot expire. It cannot restrict land use. It cannot enforce carbon limits or penalize political dissent or auto-liquidate when its holder falls out of regulatory favor.

A tokenized asset can be coded to do all of these things. Not as a hypothetical — as a documented feature that regulators and ESG compliance frameworks are actively requesting.

The World Economic Forum’s 2025 report on asset tokenization, produced in collaboration with Accenture, explicitly identifies programmability—the ability to embed compliance rules, conditional transfers, and automated governance directly into smart contracts—as a core value proposition of tokenized assets.[6] The report acknowledges what it calls the “paradox of programmability”: the same smart contract features that automate efficiency also embed constraints that limit the holder’s control over the asset.

Coffman’s usufruct definition contains a clause that now deserves its own analysis: “as long as the property is not damaged or altered in any way.”

In the Roman system, this condition was enforced by a magistrate. The occupier’s rights were conditional on compliance with the sovereign’s definition of acceptable use.

In the tokenized system, this condition is enforced by code. The programmable compliance layer does what the magistrate once did, but faster, automatically, and at global scale. Carbon limits. Land-use restrictions. Behavioral parameters. ESG scoring. The condition of occupancy is embedded in the smart contract itself.

Private property, in the Western legal tradition, is defined by what legal scholars call the bundle of rights: the right to use, exclude, transfer, encumber, and destroy. Remove any of these and you have something less than property.

Programmable tokens remove all of them conditionally, and that conditionality is controlled by whoever holds the administrator key.

When the issuer can freeze, claw back, or modify the parameters of your asset, it is not your asset. It is a revocable license, dressed in the language of ownership, enforced by code instead of a magistrate.

The mechanism has been modernized. The subjection has not.

IV. The Conqueror Controls Both Sides

Coffman described the Roman usufruct as a system in which the emperor controlled both the land and the occupier’s relationship to it. The conqueror held the estate of possession. He also set the terms of the estate of uses. He controlled both sides of the equation.

In the tokenized real-world asset system, the institutional tokenizer controls both sides simultaneously.

The token owner receives yield, income generated by the underlying asset. The tenant or occupant uses the property and pays rent, generating the income stream that produces the yield. The institutional tokenizer sits in the middle, holding legal title, controlling the smart contract, collecting management fees from both the income stream and the token issuance, and setting the conditions under which both the tenant and the token holder operate.

BlackRock’s stated ambition is to tokenize every real asset. If that ambition is realized, there is no exit into untokenized property. The entire investable universe passes through the institutional tokenizer’s custody and compliance architecture. There is no outside.

That is not a market. That is a closed system.

Technocracy has a name for this. It is called a Technate: an energy-based command economy administered by technical experts, in which all resources are managed centrally and allocated according to technical parameters rather than market prices or individual choice. The 1930s Technocracy movement was explicit about this goal. What has changed since is not the objective. What has changed is the technology available to implement it.

The tokenized real-world asset ecosystem is the Technate’s property layer. The central bank digital currency is its monetary layer. The digital identity credential is its identity layer. Together, they form a closed system in which every transaction, every occupancy, every yield payment, and every property transfer passes through infrastructure controlled by a small number of institutions operating under a regulatory charter from the sovereign above them.

V. The Hierarchy of Conquerors

BlackRock appears to be the conqueror. It is not the ultimate one.

The system has multiple conqueror layers, each extracting tribute from the layer below. Each layer above controls the layer beneath it, not with armies, but with access.

At the bottom: the tenant, paying rent, generating cash flow, holding no title.

Above the tenant: the token holder, receiving yield, believing he is an owner, holding an estate of uses.

Above the token holder: the institutional tokenizer (BlackRock, JPMorgan Onyx, Franklin Templeton, Securitize) holding legal title in custody, controlling the smart contract, governing the compliance architecture.

Above the institutional tokenizer: the regulatory sovereign (the SEC, OFAC, the Basel Committee, the Financial Stability Board), which can direct, restrict, freeze, or restructure the institutional tokenizer’s operations at any time. BlackRock does not own its position. It licenses it. When the regulatory sovereign commands, BlackRock complies. The attempt to sanction Tornado Cash’s smart contract code in August 2022 demonstrated the ambition: OFAC placed a decentralized protocol on the Specially Designated Nationals list, establishing that regulators would attempt to make code itself illegal.[7] Though the Fifth Circuit overturned that designation in November 2024 on narrow statutory grounds, the regulatory appetite was fully exposed. The institutional ecosystem adjusted its compliance architecture without resistance.

Bank for International Settlements.

The BIS is not a treaty organization. It is not a democratic institution. It was formally created on February 27, 1930, as a limited liability company incorporated under Swiss law, with member central banks as shareholders.[8] It pays dividends. It holds assets. It enjoys absolute immunity from Swiss jurisdiction and from every national legal system under the Headquarters Agreement concluded with the Swiss Federal Council on February 10, 1987.[9]

No court can compel it. No government can audit it without its consent. No treaty supersedes its operational independence.

The BIS sets binding rules for every regulated bank in every member jurisdiction through the Basel capital framework. These are not suggestions. Comply or be excluded from the global correspondent banking system. The BIS does not enforce compliance with armies. It enforces it with access. This is more effective than military conquest because it is invisible, technical, and appears to be nothing more than prudent financial regulation.

The BIS Innovation Hub is building the monetary substrate for the entire tokenized property ecosystem: Project Agorá, Project Mariana, Project Dunbar, and the Unified Ledger concept.[10] When complete, every CBDC, every tokenized deposit, and every tokenized real-world asset will settle through the infrastructure that the BIS designed and governs.

BIS General Manager Agustín Carstens made the agenda explicit at an IMF seminar on October 19, 2020: “A key difference with a CBDC is that the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability. And also, we will have the technology to enforce that.”[11]

You cannot fully own a tokenized asset purchased with money that can be switched off.

The BIS is the Ultimate SovCorp, the emperor whose name does not appear on the land grant, but without whose authority no land grant is valid.

VI. The Proof of Concept Is Running

The usufruct system requires a predicate condition: the elimination of existing title. You cannot tokenize contested property. You need a clean slate, a jurisdiction where prior ownership claims have been erased, suspended, or deemed invalid by sovereign authority.

Gaza provided that condition.

The reconstruction framework for Gaza — documented across the Board of Peace, Project Sunrise, and affiliated Gulf sovereign wealth structures — represents the first full-scale deployment of a tokenized governance model applied to land and resource rights in a post-conflict territory. The principals are public: Jared Kushner, Steve Witkoff, Tahnoun bin Zayed of Abu Dhabi’s Royal Group, and the sovereign wealth ecosystems of the UAE and Saudi Arabia. The affiliated tokenization infrastructure includes World Liberty Financial and its USD1 stablecoin, backed by Tether reserves and Gulf sovereign capital.

The model is straightforward. Sovereign authority tokenizes land and resource rights. It issues yield-bearing tokens to investors. It administers the territory through a technocratic governance layer. Residents receive digital identity credentials and programmable benefit tokens. Not deeds. Not title. Programmable access — conditional on compliance with parameters set by the governing authority.

This is not a conspiracy theory. The principals named themselves. The governance architecture is documented. The capital flows are traceable.

It is also not new. It is Roman. The emperor seizes the territory of a conquered kingdom. He considers the land public. He rents it — ususfructus — to his soldiers and settlers. He retains the estate. They receive the estate of uses.

Coffman described the Wildlands Project as Stage One of this system applied to American land through regulatory usufruct. Gaza is Stage Three applied in real time to a post-conflict territory — with digital identity, programmable currency, and tokenized property rights replacing the regulatory overlay with something far more comprehensive and far more difficult to escape.

When the model works in a controlled environment, it gets scaled. Ukraine reconstruction documents reference similar frameworks. NEOM and associated smart city projects integrate tokenized land administration explicitly. The proof of concept is running. The scale-up is funded.

The Verdict

The evidence is not ambiguous, and the conclusion is not speculative.

Real-world asset tokenization, as designed and deployed by the actual institutions with actual capital in actual regulatory frameworks, is a digital implementation of the Roman usufruct — updated for the twenty-first century with programmable smart contracts, biometric identity credentials, CBDC monetary rails, and a regulatory compliance architecture that closes every exit.

The original owner is displaced altogether and reappears as a tenant.

The token holder is not an owner. He is a usufructuary, holding an estate of uses while the estate of possession remains with the institutional administrator above him.

The tenant is not a renter in a free market. He is a productive occupant in a hierarchical system where the terms of his occupancy are set by an institution that also controls the token holder above him.

The institutional tokenizer is not a market intermediary. He is a provincial governor — holding title in custody, issuing yield tokens to the investor class, collecting rent from the occupant class, and governing the province under a charter from the regulatory sovereign above him.

The regulatory sovereign is not a neutral referee. He is a layer of the conquering hierarchy — setting the rules under which the governor operates, enforcing compliance with access rather than armies, and answering ultimately to the BIS above him.

The BIS is the emperor. It holds no land directly. It issues no currency directly. But without its monetary framework, no currency is valid. Without its capital standards, no bank operates. Without its settlement infrastructure, no tokenized asset can clear. It retains the ultimate estate in the global monetary system, and from that position, it controls everything that depends on monetary access. Everything does.

Private property is not being seized. It is being converted — from a right into a subscription. From dominion over a thing to a programmable, revocable, conditional claim to yield from a thing managed by others.

The UN chose the word usufruct deliberately. Coffman found it and told us what it meant. The Technocrats have since built the digital infrastructure to implement it at a civilizational scale. And the frontier soldiers, the token holders who believe they are investors, are being settled into a system they do not yet understand, generating cash flows that ascend through every layer above them to the emperor at the top.

The emperor never left. He just incorporated.

ENDNOTES

[1] Michael S. Coffman, “Background to the Wildlands Project,” Agenda 21 News, September 18, 2014. https://agenda21news.com/2014/09/background-wildlands-project/

[2] Larry Fink, remarks at New York Times DealBook Summit, November 2022. Reported: “BlackRock CEO Says ‘Next Generation for Markets’ Is Tokenization,” Yahoo Finance, December 1, 2022. https://finance.yahoo.com/news/blackrock-ceo-says-next-generation-120411520.html

[3] Larry Fink, “2025 Annual Chairman’s Letter to Investors,” BlackRock, 2025. https://www.blackrock.com/corporate/investor-relations/larry-fink-annual-chairmans-letter

[4] BlackRock USD Institutional Digital Liquidity Fund (BUIDL), fund documentation and Securitize transfer agent agreement, 2024. See also: “BlackRock Launches First Tokenized Fund on a Public Blockchain,” BlackRock press release, March 20, 2024.

[5] Securitize, “Transfer Agent and Compliance Infrastructure,” platform documentation, 2024. Securitize serves as transfer agent for BlackRock BUIDL, Hamilton Lane SCOPE, and KKR tokenized funds.

[6] World Economic Forum and Accenture, “Asset Tokenization in Financial Markets: The Next Generation of Value Exchange,” May 2025. https://reports.weforum.org/docs/WEF_Asset_Tokenization_in_Financial_Markets_2025.pdf

[7] U.S. Department of the Treasury, Office of Foreign Assets Control, designation of Tornado Cash, August 8, 2022 (SDN List). Subsequently: Van Loon et al. v. Department of the Treasury, U.S. Court of Appeals, Fifth Circuit, November 26, 2024 (designation overturned on statutory grounds). OFAC delisted Tornado Cash on March 21, 2025.

[8] Bank for International Settlements, formally established Rome, February 27, 1930, under the Hague Agreement of January 20, 1930; incorporated as a limited liability company under Swiss law. See: BIS, “Legal information,” https://www.bis.org/about/legal.htm; also BIS Profile (1999), https://www.bis.org/about/profil99.htm

[9] Headquarters Agreement between the Bank for International Settlements and the Swiss Federal Council, February 10, 1987. The Agreement confirms the BIS’s immunity from Swiss jurisdiction and from seizure. See: BIS, “Legal information,” https://www.bis.org/about/legal.htm

[10] BIS Innovation Hub, project documentation: Project Agorá (tokenized cross-border payments), Project Mariana (FX tokenization), Project Dunbar (multi-CBDC platform), and “BluePrint for the Future Monetary System,” BIS Annual Economic Report, June 2023. https://www.bis.org/publ/arpdf/ar2023e3.htm

[11] Agustín Carstens, General Manager, BIS, remarks at IMF seminar “Cross-Border Payments — A Vision for the Future,” October 19, 2020 (at 22:52). Widely reported; transcript confirmed by multiple contemporaneous sources.

Image: Source [Edited]

Original Article: https://www.technocracy.news/tokenization-of-real-world-assets-is-a-tool-of-conquest-not-liberation/

![Fauci Pleads The Fifth 111 Times | Trump Calls Operation Warp Speed [Genocide] A 'Spectacular Success' And Pretends He Was Against Fauci, Despite Him Giving Fauci A Commendation For His Work + Respecting Biden's Pardon](https://cdn.getmidnight.com/0b0f9daf495199bed1eaf719adc55c4f/size/w600/2026/07/13297b15-9b1e-425b-99d2-24b1659a3c2a_6000x4000.jpg)

Comments ()